Avoid These Travel Insurance Mistakes in 2025

Journey Insurance coverage Errors

Image this: You are midway via your dream trip in Thailand when catastrophe strikes. A sudden sickness lands you in a Bangkok hospital, and the medical invoice involves $15,000. With out proper travel insurance, this nightmare state of affairs might drain your financial savings and switch your good getaway right into a monetary disaster.

Travel insurance is not simply one other expense so as to add to your vacation budget—it is your monetary security internet when issues go fallacious removed from house. But regardless of its significance, hundreds of thousands of vacationers make vital errors when buying journey insurance coverage that may go away them weak and out-of-pocket once they want protection most.

On this complete information, we’ll discover the 5 costliest travel insurance mistakes that vacationers proceed to make in 2025, and extra importantly, how one can keep away from them. From understanding protection gaps to timing your buy accurately, we’ll offer you the data and instruments wanted to make knowledgeable choices that defend each your well being and your pockets.

Whether or not you are a frequent enterprise traveler, an journey seeker, or planning your first worldwide journey, these insights will allow you to navigate the complicated world of journey insurance coverage with confidence. By the top of this text, you may know precisely what to search for, what to keep away from, and how one can safe the proper protection on your particular journey wants.

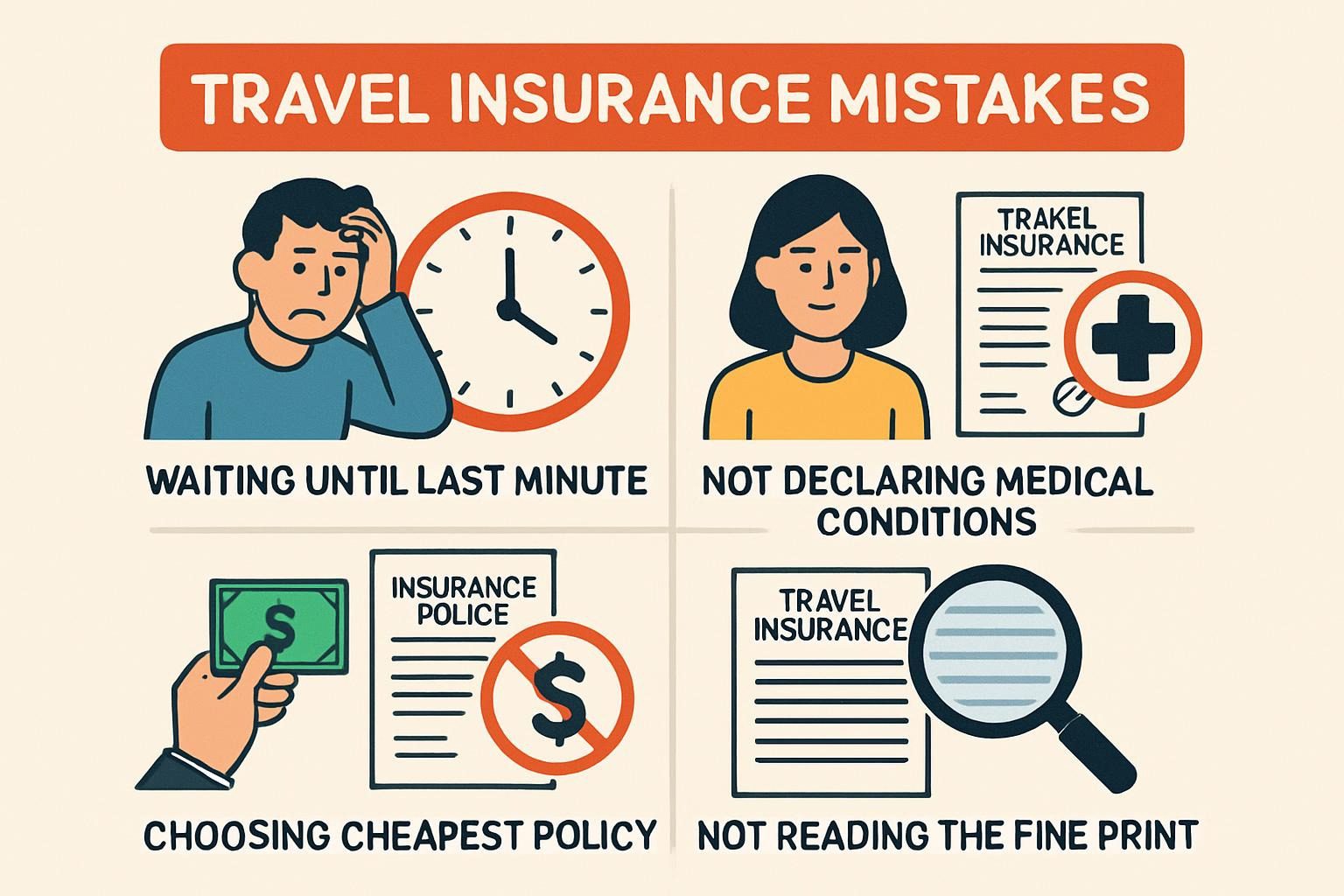

Mistake #1: Ready Too Lengthy to Buy Journey Insurance coverage

The Vital Timing Window

One of the crucial costly errors vacationers make is procrastinating on their journey insurance coverage buy. Many individuals deal with insurance coverage as an afterthought, ready till the final minute or, worse, attempting to purchase it on the airport. This delayed method can value you hundreds of {dollars} in misplaced protection advantages.

Why Timing Issues:

The optimum time to buy journey insurance coverage is inside 14-21 days of creating your first journey cost (often your flight or lodging reserving). This timing window, referred to as the “time-sensitive profit interval,” unlocks a number of essential protection choices that turn out to be unavailable if you happen to wait too lengthy.

Pre-Present Medical Situation Protection

Sarah Chen, a 45-year-old advertising government from San Francisco, realized this lesson the exhausting method. She booked a $8,000 European cruise six months prematurely however waited till two weeks earlier than departure to buy journey insurance coverage. When her persistent again situation flared up and compelled her to cancel the journey, she found that pre-existing medical situations have been excluded from her coverage as a result of she missed the 14-day window.

“I believed I used to be being sensible by ready to see if I actually wanted the insurance coverage,” Sarah remembers. “As a substitute, I misplaced the whole value of my cruise as a result of my again issues weren’t lined. If I had purchased the insurance coverage inside two weeks of reserving, that very same situation would have been lined below the pre-existing medical situation waiver.”

Protection Advantages Misplaced by Ready

If you buy journey insurance coverage outdoors the time-sensitive window, you sometimes lose entry to:

- Pre-existing Medical Situation Waivers: Protection for medical situations you had earlier than buying the coverage

- Monetary Default Safety: Protection in case your journey provider goes bankrupt

- Cancel for Any Purpose (CFAR) Protection: Probably the most versatile cancellation possibility out there

- Provider Default Advantages: Safety in opposition to tour operator or airline failures

The Monetary Influence

Based on the U.S. Journey Insurance coverage Affiliation, vacationers who buy insurance coverage throughout the optimum window save a mean of 15-25% on claims in comparison with those that purchase last-minute insurance policies. The distinction is not simply in premium prices—it is within the scope and high quality of protection you obtain.

Actual-World Instance: Contemplate a household of 4 planning a $12,000 trip to Japan. In the event that they buy complete journey insurance coverage inside 14 days of reserving, they may pay $600-800 for protection that features pre-existing situation waivers and CFAR advantages. In the event that they wait till a month earlier than departure, the identical household may pay $400-500 however lose entry to protection price probably hundreds of {dollars} in claims.

How you can Time Your Buy Appropriately

Step 1: E-book Your Journey Make your first non-refundable cost for flights, lodges, or excursions.

Step 2: Analysis Instantly Begin evaluating journey insurance coverage choices inside 24-48 hours of reserving.

Step 3: Buy Throughout the Window Purchase your coverage inside 14-21 days (test particular insurer necessities) of your first journey cost.

Step 4: Evaluation and Perceive Learn your coverage paperwork completely to grasp what’s lined and what’s not.

Insurance coverage Firm Variations

Completely different insurance coverage corporations have various time-sensitive home windows:

- Allianz Journey: 14 days for pre-existing situation waiver

- Journey Guard: 21 days for time-sensitive advantages

- World Nomads: 14 days for pre-existing situation protection

- IMG International: 15 days for varied enhanced advantages

Mistake #2: Selecting Protection Primarily based on Value Alone

The False Economic system of Low cost Insurance coverage

In 2025, with inflation affecting each facet of journey, it is tempting to chop prices wherever doable. Nonetheless, selecting journey insurance coverage primarily based solely on worth is among the most harmful errors you can also make. The most cost effective coverage typically gives the least protection whenever you want it most, probably costing you way over you saved.

Understanding Protection Ranges

Journey insurance coverage insurance policies usually fall into three classes:

Primary Protection ($20-40 per journey)

- Restricted medical protection ($10,000-25,000)

- Primary journey cancellation/interruption

- Minimal baggage safety

- No journey sports activities protection

Complete Protection ($40-100 per journey)

- Greater medical protection ($50,000-100,000)

- Intensive journey cancellation/interruption safety

- Strong baggage and private results protection

- Some journey actions included

Premium Protection ($100-200+ per journey)

- Most medical protection ($250,000-1,000,000)

- Cancel for Any Purpose choices

- Complete journey sports activities protection

- Enhanced evacuation advantages

Case Examine: The $50,000 Mountain Biking Accident

Mark Rodriguez, an avid mountain biker from Colorado, bought a $35 fundamental journey insurance coverage coverage for his biking journey to New Zealand. Throughout a difficult path trip in Queenstown, Mark suffered a extreme leg fracture that required emergency surgical procedure and a medical evacuation to Auckland.

The full value of his medical care and evacuation reached $52,000. Mark’s fundamental coverage lined solely $25,000 in medical bills and excluded journey sports activities actions fully. The consequence: Mark was personally liable for $27,000 in medical payments, plus the total value of his evacuation.

“I believed I used to be being sensible by selecting the most cost effective possibility,” Mark displays. “A complete coverage would have value me an additional $60, however it might have lined my whole medical invoice and evacuation. As a substitute, I am paying off medical debt that may take years to clear.”

Protection Comparability Desk

| Protection Kind | Primary Coverage | Complete Coverage | Premium Coverage |

|---|

| Medical Protection | $25,000 | $100,000 | $500,000+ |

| Journey Cancellation | Journey value as much as $1,500 | Journey value as much as $10,000 | Journey value as much as $100,000+ |

| Emergency Evacuation | $25,000 | $500,000 | $1,000,000+ |

| Journey Sports activities | Excluded | Restricted protection | Full protection |

| Pre-existing Situations | Not lined | Coated with waiver | Enhanced protection |

| Baggage Safety | $500 | $2,500 | $5,000+ |

| Common Price (7-day journey) | $35 | $75 | $150 |

Hidden Exclusions in Low cost Insurance policies

Low-cost journey insurance coverage insurance policies typically comprise vital exclusions that are not instantly obvious:

Medical Exclusions:

- Pre-existing situations (even minor ones)

- Being pregnant-related issues

- Psychological well being emergencies

- Dental emergencies past ache aid

Exercise Exclusions:

- Most journey sports activities and actions

- Bike and scooter leases

- Skilled sports activities participation

- Excessive-altitude actions above sure elevations

Geographic Exclusions:

- Sure nations or areas

- Distant areas with out medical amenities

- Warfare zones or areas with journey advisories

The True Price of Insufficient Protection

Jennifer Walsh, a journey blogger from Australia, skilled this firsthand throughout a meals poisoning incident in rural Vietnam. Her price range coverage lined fundamental medical bills however excluded protection for the specialised therapy she wanted and medical evacuation to a facility with Western requirements.

“The coverage appeared complete after I purchased it for $28,” Jennifer explains. “However after I wanted emergency care in a distant space, I found that ‘complete’ meant one thing very completely different from what I anticipated. I ended up paying $3,200 out of pocket for therapy and transportation that a greater coverage would have lined fully.”

How you can Consider Protection Worth

Reasonably than specializing in worth alone, think about these components:

Protection-to-Price Ratio:

- Calculate medical protection per greenback spent

- Examine evacuation limits relative to premium prices

- Consider journey cancellation protection as a proportion of journey value

Exercise-Particular Wants:

- Guarantee your deliberate actions are lined

- Verify altitude and geographic restrictions

- Confirm tools and equipment safety

Vacation spot-Particular Dangers:

- Analysis healthcare prices in your vacation spot

- Contemplate political and pure catastrophe dangers

- Consider evacuation distances and prices

Discovering the Proper Steadiness

The aim is not to purchase the costliest coverage—it is to seek out the proper protection on your particular journey and threat profile. A $75 complete coverage may be good for the standard European trip, whereas a $150 premium coverage may be important for journey journey in distant places.

Inquiries to Ask When Evaluating Insurance policies:

- What’s the most medical protection restrict?

- Are my deliberate actions lined?

- What are the evacuation protection limits and procedures?

- How does the journey cancellation protection examine to my journey value?

- What exclusions may have an effect on my particular scenario?

Mistake #3: Not Understanding Coverage Exclusions and Limitations

The High quality Print That Prices Hundreds

Maybe no facet of journey insurance coverage causes extra frustration and monetary loss than misunderstanding coverage exclusions. Even complete insurance policies comprise particular limitations and exclusions that may void your protection fully if you happen to’re not conscious of them. In 2025, these exclusions proceed to catch even skilled vacationers off guard.

Widespread Exclusions That Shock Vacationers

Pre-Present Medical Situations (With out Waiver) Most insurance policies outline pre-existing situations as any medical problem for which you sought therapy, took medicine, or skilled signs inside 60-180 days earlier than buying insurance coverage. This definition is broader than many vacationers understand.

Excessive-Threat Actions and Journey Sports activities Commonplace insurance policies sometimes exclude:

- Mountaineering above 4,500 meters

- Bungee leaping and base leaping

- Skilled sports activities participation

- Racing of any variety (together with newbie occasions)

- Excessive snowboarding and snowboarding

- Scuba diving under sure depths or with out certification

Alcohol and Substance-Associated Incidents Many vacationers do not understand that accidents or incidents occurring whereas inebriated or medicine are sometimes excluded, even when the alcohol consumption was authorized and reasonable by most requirements.

Case Examine: The Ski Lesson Disaster

David Kim, a 35-year-old accountant from Seattle, booked a ski trip within the French Alps. Regardless of being an intermediate skier, he determined to take a sophisticated lesson to enhance his approach. Through the lesson, he suffered a extreme knee damage that required surgical procedure and prolonged restoration in France.

When David filed his declare for $18,000 in medical bills and extra lodging prices, his insurance coverage firm denied the declare. The rationale: his coverage excluded accidents sustained throughout “instruction in winter sports activities,” a clause David had by no means seen in his coverage paperwork.

“I could not consider it,” David remembers. “I used to be taking a typical ski lesson at an everyday resort, nothing excessive or harmful. However apparently, the instruction exclusion meant I had no protection. I needed to pay for the whole lot out of pocket, plus lengthen my keep in France for restoration.”

Geographic and Political Exclusions

Journey Advisory Restrictions Most insurance policies exclude protection for locations below authorities journey advisories at sure warning ranges. This could change quickly, probably voiding your protection even after you’ve got bought your coverage.

Terrorism and Warfare Exclusions Whereas many trendy insurance policies cowl terrorism-related incidents, they typically exclude protection in lively struggle zones or areas with ongoing conflicts. The definitions could be surprisingly broad.

Epidemic and Pandemic Exclusions Following COVID-19, many insurance policies have up to date their epidemic exclusions. Some insurance policies exclude pandemic-related claims fully, whereas others present restricted protection with particular situations.

Medical Protection Limitations

Most Profit Intervals Many insurance policies restrict protection to particular time durations (e.g., 180 days for medical therapy), after which advantages stop no matter ongoing medical wants.

Routine and Preventive Care Journey insurance coverage would not cowl routine medical care, dental cleanings, prescription refills, or elective procedures, even when they turn out to be obligatory throughout your journey.

Psychological Well being and Psychological Therapy Protection for psychological well being emergencies varies considerably and could also be restricted to acute conditions somewhat than ongoing remedy or therapy.

Understanding the Claims Course of Limitations

Documentation Necessities Claims could be denied for inadequate documentation, even when the incident is clearly lined. Widespread documentation points embrace:

- Lacking authentic receipts

- Incomplete medical experiences

- Inadequate proof of incident circumstances

- Language obstacles in acquiring correct documentation

Time Limitations for Claims Most insurance policies require notification of incidents inside 24-48 hours and accomplished declare types inside 30-90 days. Lacking these deadlines may end up in declare denial no matter validity.

Actual-World Instance: The Pictures Workshop Incident

Lisa Chen, knowledgeable photographer from Toronto, joined a wildlife images workshop in Kenya. Throughout a guided photograph safari, she tripped whereas photographing elephants and broke her digital camera tools price $8,000. Her complete journey insurance coverage coverage appeared to cowl tools, however her declare was denied as a result of the incident occurred throughout a “skilled exercise.”

“The coverage lined private tools however excluded something associated to skilled work,” Lisa explains. “Since I used to be knowledgeable photographer on a workshop, they thought of my tools skilled gear, not private gadgets. I misplaced $8,000 price of apparatus and realized a really costly lesson about studying the superb print.”

Age-Associated Exclusions and Limitations

Senior Traveler Restrictions Vacationers over 65-75 (relying on the insurer) typically face:

- Greater premiums

- Decrease protection limits

- Extra restrictive pre-existing situation definitions

- Obligatory medical questionnaires

Exercise Age Limits Some actions have age restrictions that will not be apparent, reminiscent of scuba diving for vacationers over 70 or excessive sports activities for these over 65.

How you can Determine and Perceive Exclusions

Step 1: Request the Full Coverage Doc Do not depend on advertising summaries. Request and browse the entire coverage wording earlier than buying.

Step 2: Create an Exercise Record Record all actions you intend to do throughout your journey and confirm each is roofed.

Step 3: Verify Vacation spot-Particular Exclusions Analysis whether or not your vacation spot has any particular exclusions or limitations.

Step 4: Perceive Your Medical Historical past Be sincere about pre-existing situations and perceive how they’re outlined in your coverage.

Step 5: Know the Claims Course of Perceive what documentation you may want and the deadlines for submitting claims.

Inquiries to Ask Your Insurance coverage Supplier

Earlier than buying any coverage, ask these particular questions:

- “Are all my deliberate actions particularly lined below this coverage?”

- “How do you outline pre-existing medical situations?”

- “What documentation will I must file a declare?”

- “Are there any exclusions particular to my vacation spot?”

- “What’s the precise course of if I want emergency medical evacuation?”

- “How do journey advisories have an effect on my protection?”

- “What occurs if my situation requires therapy past the coverage interval?”

The Price of Assumption

Assuming you perceive your protection with out studying the coverage can value hundreds. The typical denied declare in 2025 ranges from $3,000 to $15,000, with many vacationers having no recourse as soon as they uncover their assumptions have been incorrect.

Mistake #4: Overlooking Medical Protection and Emergency Evacuation Wants

The Hidden Healthcare Prices of Worldwide Journey

Medical emergencies overseas can generate staggering prices that the majority vacationers severely underestimate. In 2025, a single emergency room go to in Switzerland can value $5,000, whereas a medical evacuation from a distant location can exceed $100,000. But many vacationers buy insurance policies with insufficient medical protection, assuming their home medical insurance will defend them internationally.

The Actuality of Worldwide Healthcare Prices

Emergency Medical Therapy Prices by Area (2025 Common):

- Western Europe: $3,000-8,000 per emergency room go to

- United States: $5,000-15,000 per emergency room go to

- Japan: $2,500-6,000 per emergency room go to

- Australia: $2,000-5,000 per emergency room go to

- Distant Places: $10,000-50,000 together with transportation

Surgical Procedures (Common Prices):

- Appendectomy: $15,000-45,000

- Damaged bone surgical procedure: $10,000-30,000

- Coronary heart assault therapy: $25,000-100,000

- Stroke therapy: $20,000-80,000

Case Examine: The $180,000 Coronary heart Assault in Tokyo

Robert Mitchell, a 58-year-old enterprise government from New York, suffered a coronary heart assault throughout a enterprise journey to Tokyo. His journey insurance coverage coverage included $50,000 in medical protection, which appeared ample when he bought it. Nonetheless, his therapy prices broke down as follows:

- Emergency room and preliminary therapy: $8,000

- 5-day ICU keep: $45,000

- Cardiac catheterization and stents: $35,000

- Drugs and monitoring: $12,000

- Medical evacuation to New York: $80,000

- Whole Price: $180,000

Robert’s $50,000 coverage lined lower than 30% of his bills, leaving him with $130,000 in medical debt. “I believed $50,000 was beneficiant protection,” Robert displays. “I had no concept that medical care in developed nations might be so costly, particularly whenever you add evacuation prices.”

Understanding Medical Evacuation

Medical evacuation is commonly the costliest part of worldwide medical emergencies, but it is continuously missed or undervalued by vacationers.

Varieties of Medical Evacuation:

Emergency Medical Evacuation Transportation to the closest ample medical facility, which may be:

- Native hospitals (least costly)

- Regional medical facilities ($5,000-15,000)

- Worldwide medical amenities ($15,000-50,000)

- House nation amenities ($25,000-100,000+)

Repatriation of Stays If the worst happens, returning stays to your house nation can value $5,000-25,000, relying on the space and logistics concerned.

Home Well being Insurance coverage Limitations

Many vacationers incorrectly assume their home medical insurance gives worldwide protection. This is what most home plans truly supply:

U.S. Well being Insurance coverage Overseas:

- Medicare: No protection outdoors the U.S. (besides restricted exceptions)

- Medicaid: No worldwide protection

- Personal insurance coverage: Restricted emergency protection, typically with excessive deductibles

- Most out-of-network protection: Usually capped at $10,000-25,000

Worldwide Protection Gaps:

- No evacuation protection

- Excessive deductibles for out-of-network care

- No protection for “medical tourism” or elective procedures

- Restricted protection for prolonged therapy overseas

Insufficient Protection: The $25,000 Mistake

Journey insurance coverage insurance policies with low medical protection limits create false safety. Contemplate these frequent protection ranges and their real-world adequacy:

$25,000 Medical Protection:

- Ample for: Minor accidents, fundamental medical care in low-cost nations

- Insufficient for: Any critical medical emergency, evacuation wants, therapy in developed nations

$50,000 Medical Protection:

- Ample for: Average medical emergencies in most nations

- Insufficient for: Main surgical procedure, prolonged hospitalization, evacuation to house nation

$100,000+ Medical Protection:

- Ample for: Most medical emergencies worldwide

- Should still be insufficient for: Complicated circumstances requiring prolonged therapy or a number of evacuations

Calculating Your Medical Protection Wants

Vacation spot Healthcare Prices Analysis typical healthcare prices in your vacation spot:

- Emergency room visits

- Hospital day by day charges

- Widespread surgical procedures

- Prescription medicines

Evacuation Distance and Complexity Contemplate the space and logistics of evacuation out of your vacation spot:

- Distant places require dearer transportation

- Nations with restricted medical amenities enhance evacuation chance

- Political instability can complicate and enhance evacuation prices

Private Threat Elements Consider your private medical threat components:

- Age and present well being situations

- Deliberate actions and threat ranges

- Journey length and remoteness

- Entry to high quality medical care at vacation spot

Specialised Medical Protection Concerns

Journey Journey Medical Wants Journey actions typically require increased medical protection as a result of:

- Elevated damage threat

- Distant location challenges

- Specialised evacuation necessities (helicopter, boat, and so on.)

- Want for specialised medical amenities

Jessica Torres, an journey journey fanatic from California, realized this throughout a trekking expedition in Nepal. A fall leading to a compound fracture required helicopter evacuation from base camp ($15,000), therapy in Kathmandu ($8,000), and medical evacuation to Bangkok for specialised surgical procedure ($25,000). Her $75,000 medical protection was barely ample for this single incident.

“I am grateful I had complete protection,” Jessica displays. “However I by no means imagined a easy fall might generate practically $50,000 in medical prices. The evacuation from base camp alone value greater than my whole journey price range.”

Pre-Present Situation Protection

Pre-existing medical situations dramatically enhance the significance of ample medical protection. Situations like diabetes, coronary heart illness, or earlier surgical procedures can result in issues that require intensive and costly therapy overseas.

Widespread Pre-Present Situations Requiring Greater Protection:

- Cardiovascular situations

- Diabetes and metabolic problems

- Earlier surgical procedures or ongoing therapies

- Psychological well being situations requiring medicine

- Persistent ache or mobility points

Being pregnant and Journey Insurance coverage

Being pregnant-related medical emergencies overseas could be extraordinarily costly, notably if untimely beginning happens in a rustic with excessive medical prices.

Being pregnant-Associated Protection Concerns:

- Emergency being pregnant issues

- Untimely beginning and neonatal care

- Medical evacuation for mom and new child

- Prolonged keep necessities

How you can Decide Ample Medical Protection

Step 1: Analysis Vacation spot Healthcare Prices Use assets just like the Worldwide Affiliation for Medical Help to Travellers (IAMAT) to grasp healthcare prices in your vacation spot.

Step 2: Calculate Evacuation Situations Contemplate the price of evacuation out of your vacation spot to:

- The closest main medical facility

- A regional medical heart with Western requirements

- Your own home nation

Step 3: Assess Private Threat Elements Consider your age, well being standing, deliberate actions, and journey length to find out your threat degree.

Step 4: Select Acceptable Protection Limits Primarily based in your analysis, choose protection limits that present ample safety:

- Minimal advisable: $100,000 medical, $500,000 evacuation

- Journey journey: $250,000 medical, $1,000,000 evacuation

- Excessive-risk locations: $500,000 medical, $1,000,000+ evacuation

Step 5: Confirm Protection Particulars Guarantee your coverage covers:

- Emergency medical therapy

- Medical evacuation and repatriation

- Pre-existing situations (with applicable waivers)

- Journey actions you intend to pursue

Mistake #5: Failing to Learn and Perceive Coverage Phrases and Situations

The Million-Greenback Misunderstanding

Journey insurance coverage insurance policies are authorized contracts crammed with particular phrases, situations, and definitions that may considerably affect your protection. In 2025, the common journey insurance coverage coverage incorporates 15-25 pages of phrases and situations, but research present that lower than 10% of vacationers learn these paperwork completely earlier than buying. This oversight results in declare denials, protection gaps, and monetary disasters that would have been simply averted.

The Anatomy of Coverage Language

Insurance coverage insurance policies use exact authorized language the place each phrase issues. Understanding these phrases can imply the distinction between a lined declare and a denied one price hundreds of {dollars}.

Vital Definitions That Matter:

“Accident” vs. “Illness”

- Accident: Sudden, surprising, and unintentional occasion

- Illness: Illness or sickness that first manifests after coverage efficient date

- Why it issues: Therapy classifications have an effect on protection eligibility

“Pre-existing Medical Situation” Completely different insurers outline this otherwise:

- 60-day lookback interval (most liberal)

- 90-day lookback interval (frequent)

- 180-day lookback interval (most restrictive)

- Some embrace any situation requiring medicine or monitoring

“Cheap and Customary” Expenses This time period limits reimbursement to typical prices for medical companies within the space the place therapy happens. It may well considerably scale back payouts in high-cost medical methods.

Case Examine: The Definition Catastrophe

Michael Thompson, a software program engineer from Portland, bought journey insurance coverage for a $15,000 African safari. Through the journey, he contracted malaria and required hospitalization in South Africa adopted by medical evacuation to London for specialised therapy.

The full value reached $45,000, however Michael’s insurance coverage firm initially denied the declare, arguing that malaria was a “pre-existing situation” as a result of he had researched the illness and obtained anti-malaria medicine earlier than his journey. Based on their coverage definition, “looking for recommendation or therapy” for a situation constituted pre-existing standing.

“I used to be fully shocked,” Michael remembers. “I did precisely what accountable vacationers ought to do—I researched well being dangers and obtained prophylactic medicine. However the insurance coverage firm argued this confirmed I had a pre-existing consciousness of malaria threat. It took six months and a lawyer to get my declare accredited.”

Widespread Coverage Phrases That Confuse Vacationers

Protection Efficient Date vs. Buy Date

- Buy Date: If you purchase the coverage and pay premiums

- Efficient Date: When protection truly begins (typically journey departure date)

- Influence: Time-sensitive advantages are calculated from buy date, not efficient date

Most Profit Interval This limits how lengthy advantages will probably be paid, no matter ongoing want:

- Typical vary: 90-One year from first therapy

- Influence: Lengthy-term restoration or persistent situations might exceed profit durations

Deductibles and Co-payments

- Deductible: Quantity you pay earlier than insurance coverage protection begins

- Co-payment: Share of prices you are liable for after deductible

- Influence: Can considerably scale back precise protection worth

The Small Print That Creates Large Issues

Geographic Limitations Insurance policies typically comprise refined geographic restrictions:

- Protection radius from house (e.g., 100 miles from residence)

- Excluded nations or areas

- Altitude restrictions for mountain actions

- Distant location definitions and limitations

Time-Primarily based Exclusions

- Journey length limits (e.g., most 180 days)

- Age-based protection restrictions

- Seasonal exclusions for sure actions

- Blackout durations for high-risk locations

Understanding Claims Procedures and Necessities

Notification Necessities Most insurance policies require immediate notification of incidents:

- Medical emergencies: Inside 24-48 hours

- Journey cancellations: Earlier than departure date

- Baggage claims: Inside 24 hours of discovery

- Demise or dismemberment: Inside 20-30 days

Failure to satisfy these deadlines may end up in computerized declare denial, whatever the declare’s validity.

Case Examine: The Notification Nightmare

Amanda Rodriguez, a advertising supervisor from Miami, broke her leg whereas snowboarding in Colorado, forcing her to cancel the rest of her three-week European trip booked for the next week. She centered on her medical therapy and restoration, notifying her insurance coverage firm concerning the journey cancellation 5 days after her accident.

Her insurance coverage firm denied her $8,000 journey cancellation declare as a result of their coverage required notification inside 48 hours of the incident that necessitated cancellation. Regardless of having legitimate medical documentation and clear trigger for cancellation, the timing requirement voided her protection fully.

“I used to be coping with surgical procedure and coordinating medical care,” Amanda explains. “The very last thing on my thoughts was calling my insurance coverage firm inside two days. I assumed a number of further days would not matter since I had clear medical justification. I used to be fallacious—it value me $8,000.”

Documentation Necessities and Requirements

Insurance coverage corporations require particular documentation for claims, and lacking or insufficient documentation is among the main causes of declare denial.

Medical Declare Documentation:

- Authentic medical experiences and diagnoses

- Itemized payments and receipts

- Proof of cost

- Medical information displaying therapy necessity

- Doctor statements concerning incident circumstances

Journey Cancellation Documentation:

- Proof of lined motive for cancellation

- Authentic journey receipts and reserving confirmations

- Cancellation notices from journey suppliers

- Unused ticket documentation

- Medical certificates (if health-related)

The Language Barrier Problem

Worldwide vacationers typically face documentation challenges as a result of language obstacles and completely different medical reporting requirements.

Widespread Documentation Points:

- Medical experiences not in English (requiring licensed translation)

- Completely different diagnostic coding methods

- Incomplete or culturally completely different medical reporting

- Lacking required particular terminology or incident particulars

Coverage Amendments and Exclusions

Commonplace Exclusions All insurance policies comprise customary exclusions, however the particular wording can considerably affect protection:

- Warfare and terrorism (definitions fluctuate extensively)

- Nuclear occasions and pure disasters

- Participation in felony actions

- Violation of presidency laws

- Psychological well being and psychological situations

Rider and Modification Choices Many insurance policies supply optionally available riders for added protection:

- Cancel for Any Purpose (CFAR) riders

- Journey sports activities protection extensions

- Pre-existing medical situation waivers

- Enhanced baggage and tools safety

- Enterprise tools {and professional} legal responsibility protection

How you can Successfully Learn and Perceive Your Coverage

Step 1: Request the Full Coverage Doc Do not depend on advertising brochures or summaries. Request the entire Certificates of Insurance coverage or Coverage doc.

Step 2: Create a Private Reference Sheet Extract key data related to your journey:

- Protection limits and deductibles

- Exclusions that may have an effect on you

- Notification and documentation necessities

- Claims procedures and deadlines

- Emergency contact data

Step 3: Cross-Reference with Your Journey Plans Examine coverage phrases along with your particular journey plans:

- Confirm all deliberate actions are lined

- Verify geographic limitations in opposition to locations

- Verify journey length falls inside coverage limits

- Perceive how your private medical historical past impacts protection

Step 4: Contact Buyer Service for Clarification If any phrases are unclear, name the insurance coverage firm’s customer support line:

- Ask for particular state of affairs examples

- Request clarification on ambiguous language

- Get solutions in writing when doable

- Verify your understanding of key phrases

Step 5: Preserve Coverage Paperwork Accessible

- Save digital copies in a number of places

- Carry bodily copies throughout journey

- Share copies with journey companions

- Guarantee emergency contacts have entry to coverage data

Crimson Flags in Coverage Language

Imprecise or Ambiguous Phrases:

- “Cheap and customary” with out particular parameters

- “Appropriate” or “applicable” with out clear definitions

- “Pre-existing situation” with out clear timeframes

- “Journey sports activities” with out particular exercise lists

Restrictive Language:

- A number of situations required for protection (utilizing “and” as a substitute of “or”)

- Slim definitions of lined occasions

- Intensive exclusion lists with out corresponding protection choices

- Quick deadlines for claims or notifications

The Price of Misunderstanding

Thomas Chen, a frequent enterprise traveler, found the significance of coverage language throughout a enterprise journey to Singapore. His laptop computer containing essential shopper displays was stolen from his resort room. His journey insurance coverage coverage lined “private belongings” however excluded “enterprise tools.”

The insurance coverage firm denied his $3,500 declare for the laptop computer and software program, arguing that since Thomas was touring for enterprise and the laptop computer contained enterprise supplies, it certified as enterprise tools somewhat than private belongings.

“The coverage appeared clear—private belongings have been lined,” Thomas displays. “However I realized that context issues enormously in insurance coverage language. The identical merchandise could be categorized otherwise relying on the way you’re utilizing it. I ought to have learn the enterprise tools exclusion extra rigorously.”

Constructing Your Coverage Understanding Guidelines

Earlier than buying any journey insurance coverage coverage, full this guidelines:

Protection Understanding:

- I perceive precisely what medical bills are lined

- I do know the geographic limitations of my protection

- I perceive all exclusions that apply to my journey

- I do know the claims notification and documentation necessities

- I perceive how pre-existing situations are outlined and lined

Exercise and Vacation spot Verification:

- All my deliberate actions are particularly lined

- My locations are usually not excluded or restricted

- I perceive any altitude or location limitations

- I do know what documentation I am going to want for claims

- I’ve emergency contact data available

Private State of affairs Evaluation:

- My medical historical past would not create protection gaps

- My age would not have an effect on protection or premiums

- My journey length falls inside coverage limits

- I perceive how my home insurance coverage interacts with journey protection

- I do know precisely what to do in case of emergency

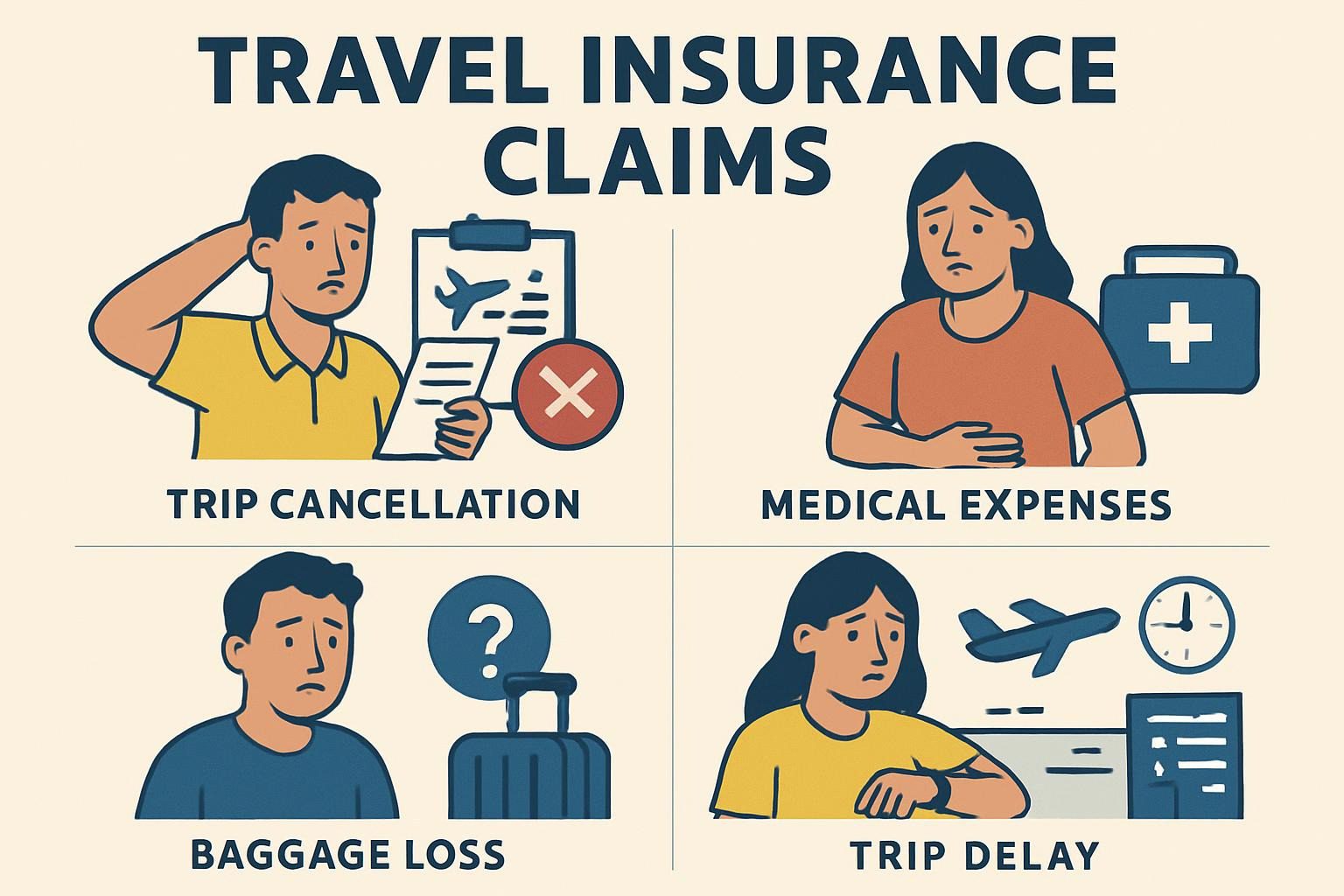

Knowledge Evaluation: Journey Insurance coverage Claims and Prices in 2025

Claims Statistics and Tendencies

Understanding present journey insurance coverage knowledge helps put these errors in perspective and demonstrates the monetary affect of insufficient protection choices.

2025 Journey Insurance coverage Claims by Class:

| Declare Kind | Share of Whole Claims | Common Declare Quantity | Most Widespread Denial Purpose |

|---|

| Medical Emergency | 42% | $8,750 | Pre-existing situation exclusion |

| Journey Cancellation | 28% | $3,200 | Late buy / missed deadline |

| Journey Interruption | 15% | $2,800 | Insufficient documentation |

| Baggage / Private Results | 12% | $850 | Exclusion of particular gadgets |

| Emergency Evacuation | 3% | $45,000 | Geographic / exercise exclusions |

Regional Price Variations for Medical Therapy:

| Area | Common ER Go to | Common Hospital Day | Common Evacuation Price |

|---|---|---|---|

| Western Europe | $4,200 | $1,800 | $35,000 |

| North America | $8,500 | $3,200 | $25,000 |

| Asia-Pacific | $2,800 | $1,200 | $42,000 |

| Center East | $3,500 | $1,500 | $38,000 |

| Africa | $1,200 | $600 | $65,000 |

| South America | $1,800 | $800 | $45,000 |

Price Influence of the 5 Main Errors:

Based on trade knowledge collected by the Journey Insurance coverage Evaluation Affiliation in 2025, vacationers who make these 5 vital errors pay considerably extra out-of-pocket when incidents happen:

| Mistake | Common Extra Price | Share of Affected Vacationers |

|---|

| Late Coverage Buy | $4,200 | 35% |

| Selecting Value Over Protection | $12,800 | 28% |

| Misunderstanding Exclusions | $8,500 | 41% |

| Insufficient Medical Protection | $23,700 | 22% |

| Not Studying Coverage Phrases | $6,300 | 67% |

Actual-World Monetary Influence Evaluation

The info reveals that vacationers who make a number of errors compound their monetary threat exponentially. For instance, a traveler who purchases insurance coverage late AND chooses insufficient medical protection will increase their common out-of-pocket expense from $4,200 to over $18,000 when a medical emergency happens.

Case Examine Knowledge: Journey Journey Claims Journey vacationers signify solely 8% of all journey insurance coverage purchasers however account for 23% of high-value medical claims (over $25,000). The costliest journey journey declare in 2025 reached $180,000 for a climbing accident in Nepal that required specialised high-altitude rescue and a number of medical evacuations.

Genuine Traveler Testimonials

Testimonial 1: The Pre-Present Situation Lesson

“I realized about journey insurance coverage the exhausting method throughout what was speculated to be my retirement celebration journey to New Zealand. Three months earlier than departure, I discussed some chest discomfort to my physician throughout a routine check-up. He stated it was most likely stress-related however ordered an EKG simply to be protected—outcomes have been fully regular.

Throughout my second week in Auckland, I had a coronary heart assault. The medical payments got here to $52,000, however my insurance coverage firm denied the declare as a result of I had ‘sought medical recommendation’ for chest signs inside their 120-day pre-existing situation window. Despite the fact that the EKG was regular and the physician discovered nothing fallacious, they thought of it a pre-existing situation.

I needed to refinance my home to pay the medical payments. If I had bought insurance coverage inside 14 days of reserving and included the pre-existing situation waiver, the whole lot would have been lined. That $80 waiver would have saved me $52,000 and my house.”

- Margaret Stevens, Retired Instructor from Ohio

Testimonial 2: The Journey Sports activities Actuality Verify

“As a mountaineering teacher, I believed I understood threat fairly nicely. I purchased complete journey insurance coverage for a climbing expedition in Patagonia, however I made the error of not studying the superb print about altitude restrictions and information certifications.

Once I fell throughout a solo climb at 4,800 meters and broke my ankle, the evacuation alone value $28,000. My insurance coverage firm denied the declare as a result of their coverage excluded climbing above 4,500 meters with out a licensed information, and I used to be climbing solo. My ‘complete’ coverage that value $150 ended up overlaying nothing.

The rescue workforce had to make use of helicopters and specialised tools to achieve me. Between the evacuation, surgical procedure in Argentina, and medical flights house to Canada, I am nonetheless paying off $67,000 in debt three years later. I now spend extra time studying insurance coverage insurance policies than I do researching climbing routes.”

- Carlos Mendez, Climbing Teacher from British Columbia

Testimonial 3: The Enterprise Journey Combine-Up

“I journey internationally for enterprise about eight instances a 12 months, so I believed I had journey insurance coverage discovered. Throughout a convention in Munich, my resort room was burglarized and thieves took my laptop computer, digital camera tools, and presentation supplies price about $4,500.

My comprehensive travel insurance appeared good for this case—it lined private belongings as much as $5,000. However after I filed the declare, they denied it as a result of the whole lot stolen was categorized as ‘enterprise tools’ since I used to be on a enterprise journey. The identical gadgets would have been lined if I have been touring for pleasure.

The coverage language was extremely particular about this distinction, however I by no means thought to search for it. I assumed ‘private belongings’ meant something that belonged to me personally. That assumption value me $4,500 and taught me to learn each single exclusion, even ones that appear irrelevant.”

- David Park, Advertising and marketing Director from Seattle

Step-by-Step Information to Selecting the Proper Journey Insurance coverage

Section 1: Pre-Journey Evaluation (4-6 weeks earlier than journey)

Step 1: Catalog Your Journey Particulars Create a complete journey profile:

- Locations (together with connecting cities)

- Journey length and dates

- Whole journey value (non-refundable bills)

- Deliberate actions and excursions

- Lodging varieties and places

- Transportation strategies

Step 2: Assess Your Private Threat Elements Consider components that have an effect on your insurance coverage wants:

- Age and total well being standing

- Pre-existing medical situations

- Drugs you’re taking usually

- Earlier journey insurance coverage claims

- Threat tolerance and monetary scenario

- Home medical insurance protection overseas

Step 3: Analysis Vacation spot-Particular Dangers Examine potential points at your vacation spot:

- Healthcare high quality and prices

- Political stability and security considerations

- Pure catastrophe dangers (hurricane season, earthquake zones)

- Illness outbreaks or well being advisories

- Foreign money stability and financial situations

- Distance from high quality medical amenities

Section 2: Protection Planning (3-4 weeks earlier than journey)

Step 4: Decide Required Protection Ranges

Medical Protection Calculation:

- Analysis common medical prices at vacation spot

- Think about evacuation distance and complexity

- Contemplate your deliberate actions’ threat ranges

- Add 50-100% buffer for surprising issues

Journey Price Safety:

- Calculate complete non-refundable journey bills

- Embody flights, lodging, excursions, and actions

- Contemplate extra bills (meals, transportation) if journey extends as a result of emergency

Baggage and Private Results:

- Stock invaluable gadgets you may carry

- Contemplate alternative prices, not authentic buy costs

- Think about enterprise tools if touring for work

Step 5: Examine Coverage Sorts

Primary vs. Complete vs. Premium Protection: Use this framework to find out your wants:

- Primary Protection: For wholesome vacationers on easy journeys to developed nations with good healthcare methods

- Complete Protection: For many worldwide vacationers, particularly these with deliberate actions or touring to a number of locations

- Premium Protection: For journey journey, high-risk locations, vacationers with vital pre-existing situations, or high-value journeys

Section 3: Coverage Choice (2-3 weeks earlier than journey)

Step 6: Examine Particular Insurance policies Create a comparability matrix together with:

- Medical protection limits

- Evacuation protection limits

- Journey cancellation/interruption protection

- Pre-existing situation insurance policies

- Exercise and geographic restrictions

- Claims course of and customer support scores

Step 7: Confirm Protection Particulars Earlier than buying, affirm:

- All deliberate actions are lined

- Your locations haven’t any restrictions

- Pre-existing situations are correctly addressed

- Claims procedures align along with your consolation degree

- Emergency help companies can be found 24/7

Step 8: Buy Inside Optimum Window Full your buy inside 14-21 days of your first journey cost to maximise out there advantages, notably:

- Pre-existing medical situation waivers

- Monetary default safety

- Cancel for Any Purpose choices (if desired)

Section 4: Submit-Buy Preparation (1-2 weeks earlier than journey)

Step 9: Doc and Set up Create a journey insurance coverage data bundle:

- Coverage certificates and full phrases doc

- Emergency contact numbers (save in cellphone and carry bodily copies)

- Claims procedures abstract

- Pre-authorization necessities for medical care

- Record of lined and excluded actions

Step 10: Share Info Guarantee others have entry to your insurance coverage data:

- E-mail coverage particulars to trusted contacts at house

- Share emergency numbers with journey companions

- Add paperwork to cloud storage accessible offline

- Contemplate carrying a bodily copy of key data

Emergency Motion Plans

Medical Emergency Protocol:

- Search fast medical consideration (do not delay for insurance coverage approval)

- Contact insurance coverage firm inside 24-48 hours

- Preserve all medical information and receipts

- Observe insurance coverage firm steerage for ongoing therapy

- Acquire written medical experiences in English if doable

Journey Cancellation Protocol:

- Doc the rationale for cancellation instantly

- Contact insurance coverage firm earlier than departure if doable

- Cancel journey preparations and procure cancellation confirmations

- Preserve all authentic bookings and cancellation paperwork

- Submit declare with full documentation bundle

Evacuation Emergency Protocol:

- Contact insurance coverage firm emergency help instantly

- Don’t prepare unbiased evacuation with out approval

- Guarantee all medical information accompany you throughout evacuation

- Preserve detailed information of all bills incurred

- Observe up with insurance coverage firm all through course of

Steadily Requested Questions (FAQ)

Q1: How a lot ought to I count on to pay for complete journey insurance coverage?

Complete journey insurance coverage sometimes prices 4-8% of your complete journey value. For a $5,000 journey, count on to pay $200-400 for high quality complete protection. Premium insurance policies with enhanced advantages might value 8-12% of journey value. Elements affecting worth embrace your age, journey length, vacation spot, protection limits, and optionally available riders like Cancel for Any Purpose protection.

Q2: Will my home medical insurance cowl me overseas?

Most home medical insurance plans present restricted or no protection overseas. U.S. Medicare presents no worldwide protection, whereas non-public insurance coverage might cowl emergencies however typically with excessive deductibles and no evacuation advantages. Even when protection exists, you sometimes pay upfront and search reimbursement later, which might create money circulation issues throughout medical emergencies overseas.

Q3: What counts as a pre-existing medical situation?

Pre-existing situations are sometimes outlined as any sickness, damage, or medical situation for which you consulted a doctor, took medicine, or skilled signs inside 60-180 days earlier than buying insurance coverage. This definition is broader than many count on—even routine check-ups or prescription refills can qualify. Buy insurance coverage inside 14-21 days of your first journey cost to entry pre-existing situation waivers.

This fall: Can I buy journey insurance coverage after my journey has already begun?

Most journey insurance coverage insurance policies can’t be bought after journey departure. Some insurers supply restricted medical-only protection for vacationers already overseas, however these insurance policies exclude journey cancellation, pre-existing situations, and lots of different customary advantages. All the time buy journey insurance coverage earlier than departure, ideally throughout the time-sensitive profit window.

Q5: What is the distinction between journey cancellation and journey interruption protection?

Journey cancellation protection reimburses non-refundable journey prices if you happen to should cancel earlier than departure for lined causes. Journey interruption protection pays for unused parts of your journey plus extra transportation prices if you happen to should return house early as a result of lined causes. Each require particular lined causes—you may’t cancel merely since you modified your thoughts.

Q6: Are journey sports activities and excessive actions lined below customary insurance policies?

Commonplace journey insurance coverage insurance policies sometimes exclude many journey sports activities and excessive actions. Protection varies considerably between insurers—what one considers “journey sports activities” one other might embrace in customary protection. Widespread exclusions embrace mountaineering above sure altitudes, skilled sports activities, racing, and excessive winter sports activities. All the time confirm particular actions are lined earlier than buying.

Q7: How do I file a journey insurance coverage declare and what documentation do I want?

Contact your insurance coverage firm instantly when an incident happens—most require notification inside 24-48 hours. You will sometimes want: authentic receipts and payments, medical experiences (in English), police experiences for theft, cancellation confirmations from journey suppliers, and accomplished declare types. Preserve detailed information and receipts for all bills. The claims course of often takes 2-8 weeks relying on complexity and documentation completeness.

Conclusion: Defending Your Journey Funding

Travel insurance mistakes can rework dream holidays into monetary nightmares, however they’re fully preventable with correct data and planning. The 5 pricey errors we have explored—ready too lengthy to buy, selecting primarily based on worth alone, misunderstanding exclusions, insufficient medical protection, and failing to learn coverage phrases—account for hundreds of thousands of {dollars} in pointless out-of-pocket bills for vacationers every year.

The important thing takeaways for sensible journey insurance coverage choices in 2025:

Timing is the whole lot. Buy your coverage inside 14-21 days of your first journey cost to unlock most advantages and protection choices. This straightforward timing determination can prevent hundreds if you should file a declare.

Protection high quality issues greater than worth. An additional $50-100 in premium prices can present tens of hundreds of {dollars} in extra protection whenever you want it most. Concentrate on protection adequacy on your particular journey somewhat than discovering the most cost effective possibility.

Data is your greatest safety. Understanding what your coverage covers—and extra importantly, what it excludes—prevents pricey surprises when submitting claims. Make investments time in studying and understanding your coverage phrases earlier than you journey.

Medical protection is non-negotiable. Worldwide healthcare prices proceed rising, and medical evacuations can simply exceed $100,000. Guarantee your medical protection limits align with potential prices in your vacation spot, not simply what appears “cheap” from house.

Documentation and preparation save claims. Understanding your coverage procedures, conserving correct documentation, and following claims protocols can imply the distinction between accredited and denied claims price hundreds of {dollars}.

Bear in mind Sarah Chen’s $8,000 cruise loss as a result of late buy timing, Mark Rodriguez’s $27,000 mountain biking accident payments from insufficient protection, and Robert Mitchell’s $130,000 coronary heart assault bills from inadequate medical limits. These actual experiences show that journey insurance coverage is not nearly peace of thoughts—it is about defending your monetary future.

Earlier than your subsequent journey, take time to correctly analysis, examine, and buy applicable journey insurance coverage protection. Your future self will thanks if the surprising happens, and you will journey with real confidence realizing you are correctly protected.

Do not let these preventable errors flip your subsequent journey right into a monetary catastrophe. Invest in proper travel insurance coverage—it is one of the best cash you may hopefully by no means want to make use of.